You have 18 months

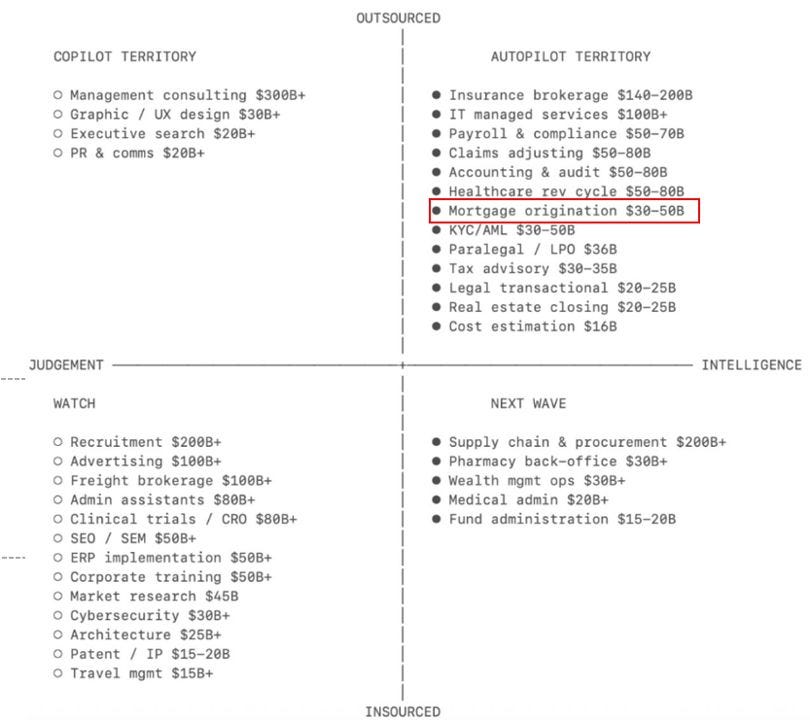

A few weeks ago, Sequoia Capital (arguably the most influential venture firm in technology, the people who backed Apple, Google, and Airbnb before the rest of us knew what any of those words meant) published a chart categorising industries by their susceptibility to AI disruption.

Mortgage origination was in the “fully AI” column.

Not “partially automated.” Not “AI-assisted.” Fully AI. Sitting there alongside insurance underwriting and paralegal work, and a handful of other professions that Sequoia’s partners apparently believe will be substantially performed by machines within a few years.

You can dismiss this, of course. Venture capitalists are paid to be dramatic. But I’ve been thinking about that chart for a while now (even posted it on LinkedIn), and it seems to me that it’s worth asking a somewhat uncomfortable question:

If you still believe the way you’re doing business today will still work in 2028, what exactly do you know that Sequoia doesn’t?

The First Billion-Dollar Originator

Someone is going to originate a billion dollars in mortgages in a single year with essentially no support staff on the sales side.

This isn’t clickbait to keep you reading. This is where I think it is going. And it scares me. And we’re making progress toward it.

But what a lot of us don’t realize is that they won’t do it by working harder. Nor will they do it by knowing more about underwriting guidelines or being better at structuring complicated files. They’ll do it because they will have a system that handles all of that automatically, accurately, at scale, and the only thing left for them to do is the thing that no machine can do: make people trust them enough to hand over the largest financial decision of their lives.

The thing that holds top producers back is inefficiencies in doing the business. It takes years to build a support team that can handle $200M a year. People quit. Workflows have to change. Expenses grow faster than revenues. It’s the classic scaling constraint. Those constraints are disappearing.

There is, of course, an unfortunate flip side to this.

The industry currently has roughly 200,000 originators.

I suspect sooner or later it will be about fifty thousand. Because once the constraints of doing high volume are removed, market share will accrue to the best. Not the best originator, but the best at generating attention and business.

I know this sounds like science fiction. But I am already watching the early version of this play out inside my own company. And if you’re paying attention to what’s moving in AI and this industry right now, the timeline is not five years. It’s not three.

It’s about eighteen months.

Doing the business, structuring, qualifying, and figuring out is becoming less relevant by the day.

Demand Generation (sales and marketing) is becoming more valuable by the day.

It’s that simple. And many, many originators have survived for a long time by being really good at ‘doing the business’. Soon, that won’t be a differentiator. And it won’t drive business. Because technology and AI are going to make everyone good at doing business.

The Superstars Are Already Here

I have originators on my team who have been in the business for a few years. They have a fraction of the product knowledge of originators with twenty years more experience.

And yet, they are superstars. One of them is going to do $100 million this year. He did $22M just 2 years ago. And they are pounding out their best purchase months ever. In February.

And the reason for this is that they understood from the beginning what most veteran originators are only now starting to reckon with: this business is no longer about being a subject matter expert in doing mortgages. It is now purely about generating business. And they spend nearly all of their time doing exactly that, marketing, relationship-building, visibility, trust, while relying on the system and the team to handle the rest. Where their more experienced colleagues spend six hours a day inside the system, structuring loans, chasing conditions, managing files, these guys spend less than one.

We haven’t reached the point of full automation, yet. But we’re at the point where it’s getting dangerous. Good enough that domain expertise in generating business is already worth more than domain expertise in doing the business.

Don’t get me wrong. Right now, this is the exception.

But within eighteen months, I believe it will be the rule. And the originators who still think their competitive advantage is their product knowledge, or years of experience, or ability to muscle a difficult file across the finish line, are going to find themselves outrun by people half their age who understood the new game before the old one was over.

Why the Smart Money Is Nervous

Around the same time that the Sequoia Capital chart came out, two pieces of writing made the rounds that, between them, changed the way people in finance were talking about AI.

The first was from Citrini Research. It was framed as a memo from June 2028 (a literary device, not a prediction) describing a world in which AI-driven productivity gains had initially fattened corporate margins before hollowing out the consumer class that those margins depended on. A negative feedback loop: companies replace workers, workers stop spending, spending decline forces more replacement. It was grim, it was speculative, and it wiped several trillion dollars off global equity markets in a matter of days. Citadel Securities published a formal rebuttal within the week. Whether or not you find Citrini’s scenario plausible (and reasonable people disagree strenuously), the fact that a Substack essay could move markets at that scale tells you something about the ambient anxiety.

The second was from Lemonade, the AI-native insurance company. This one was quieter but, I think, more instructive for our purposes. Their argument was simple and supported by public filings: as Lemonade’s revenue scales, their expenses are compressing. Not staying flat. Compressing. The traditional insurers, meanwhile, show revenue and expenses rising in lockstep, exactly as they always have. Lemonade’s explanation for this divergence was pointed: they didn’t begin as an insurance company that adopted AI. They began as an AI company that entered insurance. And that architectural difference (not a bolt-on, not a modernisation initiative, not a “digital transformation” managed by committee) is producing a fundamentally different cost curve.

Their CEO put it with admirable bluntness: “It’s not that incumbents are oblivious. It’s that they are maladapted.”

I read that line, and I thought: he might as well have been talking about the mortgage industry

The Fixed Pie

It seems to me that most of the conversation about AI in mortgage falls into one of two categories, both of which miss the point rather badly.

The first is doomsday: AI is going to replace loan originators. You’ll all be out of work. The machines are coming.

This makes for excellent LinkedIn engagement and terrible analysis. People have been getting mortgages online for twenty years. Zillow. Rocket. Better. Loan Depot. The market share gains have been, to be generous, modest. Because it turns out that when you’re making the largest financial decision of your life, you don’t want to do it the same way you purchase a pair of Nike shoes. You want to talk to a human being. And in an age of deepfakes and synthetic everything, that impulse (if anything) is getting stronger, not weaker.

The second is complacency: AI is just a tool, nothing to worry about, pass the coffee. This is equally wrong, but for subtler reasons.

What AI is going to do to mortgage, what it is already doing, for those paying attention, is not to replace the originator. It is going to obliterate the bottlenecks that currently prevent the best originators from scaling.

AI isn’t going to create more demand for mortgages. There are only a certain number of mortgages that get done each year. The question for each originator is what percentage of the fixed pie they are getting?

And I think that as the constraints for scaling (doing the business) are removed, more and more market share will accrue to the originators who are masters at demand generation. The ones who can get the most attention and build trust at scale.

And that distinction (between replacing the person and removing the constraints around the person) makes all the difference. Because when you remove bottlenecks, you don’t create equality. You create concentration. The people who were already good at the highest-value work (building relationships, generating trust, creating demand) are suddenly free to do nothing but that. And the people who defined their value by knowing how to navigate a complex process? They discover, with some discomfort, that the process is no longer complex.

But (and here is the uncomfortable part) the people who eat the new pie will not be the same people who ate the old one.

The Age of Distrust

This is why I say that the mortgage industry is entering what I’d call an age of distrust. Synthetic content is flooding every channel. AI-generated emails are becoming both indistinguishable from and distinguishable from real ones. Deepfakes exist. And borrowers are more sceptical, more guarded, hungrier for something they can actually trust than at any point in the history of the business.

And trust is the one thing AI cannot manufacture.

Which means that market share is about to flow toward the originators who can generate trust at scale. And the way you create trust is through one-to-many relationships, newsletters, social media, video, anything, really, that gives you the ability to be visible, credible, and human in a world that is becoming less of all three.

As I mentioned before, the industry currently has roughly 200,000 originators. I suspect sooner or later, it will have about 50,000 because the best at demand generation will be unleashed from the constraints of doing the business.

Which means that the 80/20 rule that has dominated this industry for years is about to become the 98/2 rule, and the two percent will not be the most knowledgeable. They will be the most visible. The most trusted. The most relentlessly, creatively, authentically present.

The subject matter expertise that took twenty years to accumulate is now being compressed into a tool that a young originator can query in seconds. But what cannot be compressed is the ability to make people feel safe.

And you have 18 months to decide which one of those you want to be.

Which brings me to the question I think matters most right now.

The Company Question

Am I at a company that is designed to let me benefit from this shift, or one that is designed to resist it?

Because here is what I’ve come to believe: it doesn’t matter how talented you are at generating business if the company you’re working for pulls you back into operations every time volume ticks up. You can be the best demand generator in the country and still drown if your system requires you to be the hero who holds everything together.

There are, broadly speaking, two kinds of mortgage companies operating right now.

The first (and this includes most of the large incumbents) is an old architecture with AI bolted on. They have legacy systems that consume the majority of their IT budgets. They have entrenched processes that were optimised for a world that is rapidly ceasing to exist, with layers of management whose continued employment depends, at some level, on the perpetuation of complexity. They employ talented people. But their structure makes genuine transformation nearly impossible, for the same reason that you cannot turn an ocean liner by asking the passengers to lean.

Can incumbents adopt AI and maintain their position? Perhaps. But the reasons to doubt it are structural, not intellectual. Lemonade’s CEO put it devastatingly: their entire organisation (hiring, incentives, technology, culture) evolved for a different environment. Asking them to become AI-native is like asking a polar bear to live its best life in the Sahara. The bear is a magnificent animal. The problem is the habitat.

The second kind of company is one that was either born AI-native or was forced by circumstance to rebuild itself from the ground up. A company like this carries none of the legacy weight. It can design its systems for the world that’s arriving rather than the world that’s departing. And the cost difference between those two architectures is not marginal. It is categorical.

I know this because I lived it. When Princeton exited the wholesale channel in 2022, it felt like a catastrophe. We were 80% wholesale and 20% retail. I was wrong. It was, in hindsight, a great strategic advantage. It gave us the chance to rebuild from the studs and to ask the question I posed publicly at a Housing Wire conference in early 2023: if you were starting a mortgage company today, knowing what you know, what would you build?

That question led to everything we’ve done since. And the answer looks nothing like what existed before.

The Gap Is Widening. Fast.

Here is what I need you to understand about timing.

The gap between companies that enable their originators to spend their time generating business and companies that suck their originators back into operations every time volume picks up has historically been small. You could argue about basis points and comp structures, but the fundamental experience of doing the work was roughly similar everywhere.

That is no longer true. And the distance is widening very, very fast.

I am watching it happen in real time. I brought on significant new volume recently and hired one additional person. One. Companies operating on legacy architecture are bringing on the same volume and having to add hundreds of thousands of payroll to support it. Not to mention creating the cascading operational drag that pulls their best originators right back into the machine. I’m hearing this from recruits right now: Their company is adding originators and ops staff, and it’s jamming up ops. Turn times, service levels, the whole thing.

The cost structures are also diverging, the originator experience is diverging, and once a company or originator falls far enough behind on this curve, I am not sure there is a way back.

Which is right now, today, you need to be with a company that is ahead of this curve.

A company where you can spend more of your time generating business and less of your time doing it. A company that has a radically low cost per funded loan, not because it skimps on quality (quite the opposite; as Deming taught us in my last newsletter, quality is what drives cost down), but because its workflows, its automations, its entire architecture were designed for a world in which AI does the cognitive heavy lifting and humans do the irreplaceable work of building trust.

And as I’ve mentioned several times already in this newsletter, the people I talk to who are building this technology (and I talk to them every day) believe the bulk of the shift happens in the next eighteen months.

Because after that, the difference between companies that are ahead of this curve and companies that are behind it will not be a matter of basis points or comp plans or whether your manager is nice.

It will be a matter of survival.

What I Want

I’ve been writing this newsletter for a while now, and I’ll confess that part of my motivation has always been to demonstrate something I believe deeply: that putting your thinking out into the world, consistently and honestly, is the single most powerful form of demand generation that exists. For me, this is not a marketing tactic. It’s a way of operating. And the originators who figure this out before the bottlenecks fully disappear are going to have a head start that may prove insurmountable.

This is why I help originators at Princeton do the same thing. Because I’ve seen what happens when you remove the constraints, when you unleash people from the misery of doing the business and let them do what they were built to do.

The billion-dollar originator is coming.

Someone will originate a billion dollars a year. They will do it with essentially no support staff on the sales side, because the system will do the rest. They will not be the most experienced person in the industry. They will be the most trusted.

The only question is whether that person will be working with you, against you, or will be you.

I want that person to be you.

Rich Weidel III

CEO, Princeton Mortgage