Too big to help

Why the big mortgage companies can't help originators anymore

“Bigger is better.”

Is it?

For years, I’ve heard this. From originators. From executives at companies with thousands of employees and billions in assets. And I confess, I started to wonder if it might be true. Am I playing a game where the cards are already stacked against me? More capital. More people. Better tech. And that seductive phrase that sounds so scientific, so irrefutable: “Economies of Scale.”

And then several lenders went public.

I felt like a kid who’d just been handed his rival’s diary. Suddenly, the financials were there for anyone to read—quarterly, audited, unavoidable.

Charlie Munger famously called profits “the scoreboard.” And to my considerable relief, when I finally got to check the scoreboard, the dog’s bark was bigger than its bite.

Now that I can dissect these financials each quarter, I’ve learned two things worth knowing:

They don’t have any meaningful economies of scale. And they don’t seem to be able to adapt to the current market, even after four years in.

Change is the Only Thing That’s Certain

Every year for the last thirty years, we’ve heard: “The mortgage industry is about to be transformed.”

Every year there’s some new company, some new model, some new technology that’s going to “disrupt” everything. The word disruption itself has been so thoroughly disrupted that it’s lost all meaning.

And nothing fundamental has changed.

I became immune to it. I focused instead on the things within my control: operational excellence, culture, pricing. The boring stuff that doesn’t make conference keynotes but does make businesses work.

But I’m beginning to believe that this time is different. Not because anyone told me so—I’ve learned to ignore that kind of talk. I’m beginning to believe it because of what we’ve been able to accomplish. Problems that plagued us for years are now fixed. And the way they got fixed tells me something important about what’s coming.

Numbers Don’t Lie

It started, of all places, in our accounting department.

When the market turned in 2022, we started bleeding cash. And I quickly learned the meaning of that old adage: “Accounting is the language of business.” I had always assumed I was fluent. It turns out I was barely conversational.

We had a full accounting team, CFO, Controller, accounts payable, staff accountants, payroll processing. Around $1.25M in payroll. Not cheap. And yet every time I asked a question that should have been simple (”Why are we losing money? Where exactly?”), it would take two weeks to get an answer. And it was about fifty-fifty whether they were right.

So I fired my CFO and dug in myself.

What I found was remarkable. Everything was manual. Different data sets, each maintained separately. Analysis done on spreadsheets that took hours to build and seconds to break. Charts of accounts that were essentially black boxes—money went in, mystery came out.

Everyone blamed the system. And they were right. The system was broken. But the problem was that nobody working within the system had any idea what to do about it. The only solution anyone could propose was this: “Rich, if you want more granular detail and quicker reporting, you are going to have to hire more people.”

Hire more people. We were losing money and already spending over a million dollars a year on accounting payroll.

I’m a believer that scarcity is the mother of invention. And so we got to work building a proprietary execution layer to sit on top of our existing accounting software. We didn’t build it to sell to anyone. It was a lot of brain damage, but only $25K in actual programming costs.

The result? Ten times better output. Seventy-five percent reduction in accounting payroll.

This was my moment of clarity.

If we could do it for accounting—an area where I had no particular expertise and certainly no passion, could we do the same thing for the thing we actually know how to do? Could we do it for mortgage manufacturing?

There’s a useful framework from a 1973 book called Small Is Beautiful by E.F. Schumacher. In a passage about corporate organization, he wrote something that’s stayed with me:

“Without order, planning, predictability, central control, accountancy, discipline—without these nothing fruitful can happen, because everything disintegrates. And yet—without the magnanimity of disorder, the happy abandon, the entrepreneurship venturing into the unknown and incalculable, without the risk and the gamble, the creative imagination rushing in where bureaucratic angels fear to tread—without this, life is a mockery and a disgrace.”

Large organizations have become extraordinarily good at the first part. They’ve built entire departments devoted to order and control. What they’ve lost (or perhaps never had in the first place) is the ability to move quickly, to experiment, to adapt.

I had a call with a friend who runs a top 20 lender a few weeks ago. He was throwing around huge numbers—locks, fundings, number of originators. I couldn’t help it. I felt envious. The scale. The resources. The optionality that comes with size.

And then I shared what we were doing. Our thin margins. Our cost per funded loan.

And he said something I didn’t expect: “Sometimes I wish I were in your seat. You can get done in four months what takes me three years.”

Suddenly I wasn’t so envious.

Here’s what else he said, and I find myself agreeing: “For the first time since 2008, there is real differentiation between mortgage companies emerging. The majority of current companies are not going to be able to make the operational and technology transitions over the next two to three years. Look at the leadership teams. They just don’t have the skills for this new world. They’re going to slowly lose originators and market share because their business model will become less competitive each quarter.”

The elephants, it turns out, can’t dance. Not because they lack talent, but because the very size that once protected them has become the thing that holds them back.

Don’t believe me? That’s O.K. Ask Warren Buffet

The K-Shaped Mortgage Economy

What does all this mean for you?

I think we’re seeing what amounts to a K-shaped economy emerging in mortgage. Some companies—regardless of size, but particularly smaller ones with entrepreneurial leadership—are adapting rapidly and gaining significant operational advantages. Others are going in the opposite direction: accumulating costs and complexity while their productivity per person continues to decline.

But here’s where I want to be careful. The K isn’t just about companies. It’s about originators.

The top producers of the past were subject matter experts. They knew how to do hard loans. They were disciplined. They micromanaged their files with an attention to detail that bordered on obsession. And for decades, those skills were the difference between success and mediocrity.

Those skills are becoming commoditized.

I’ve seen prototypes of what AI can do for loan processing. Things that would have seemed like science fiction three years ago. I understand why most originators are skeptical—we’ve heard “this will change everything” too many times. But I’ve seen it and we’re doing it. And it’s coming faster than most people expect.

Here’s what I think is going to happen: More market share is going to be won by originators who are master marketers.

There are top producers today who have almost no social presence. They’ve built their businesses on referrals, relationships, and raw competence. And that’s served them well. But the top producers of tomorrow? They’re the ones who today are mastering social media. It’s a gold rush. And like all gold rushes, the early arrivals will stake the best claims.

And they aren’t doing it alone. The smartest ones have teams behind them: copywriting, logistics, video editing, even PR. They’re not posting five-star reviews and pictures from the closing table. They’re creating content that attracts people to them without ever having to sell.

There’s an old distinction in marketing between persuasion and attraction. Persuasion is when you make your case and try to convince someone. Attraction is when you become the kind of thing people want to come to on their own. The best originators I know are learning that attraction beats persuasion every time.

The Time Question

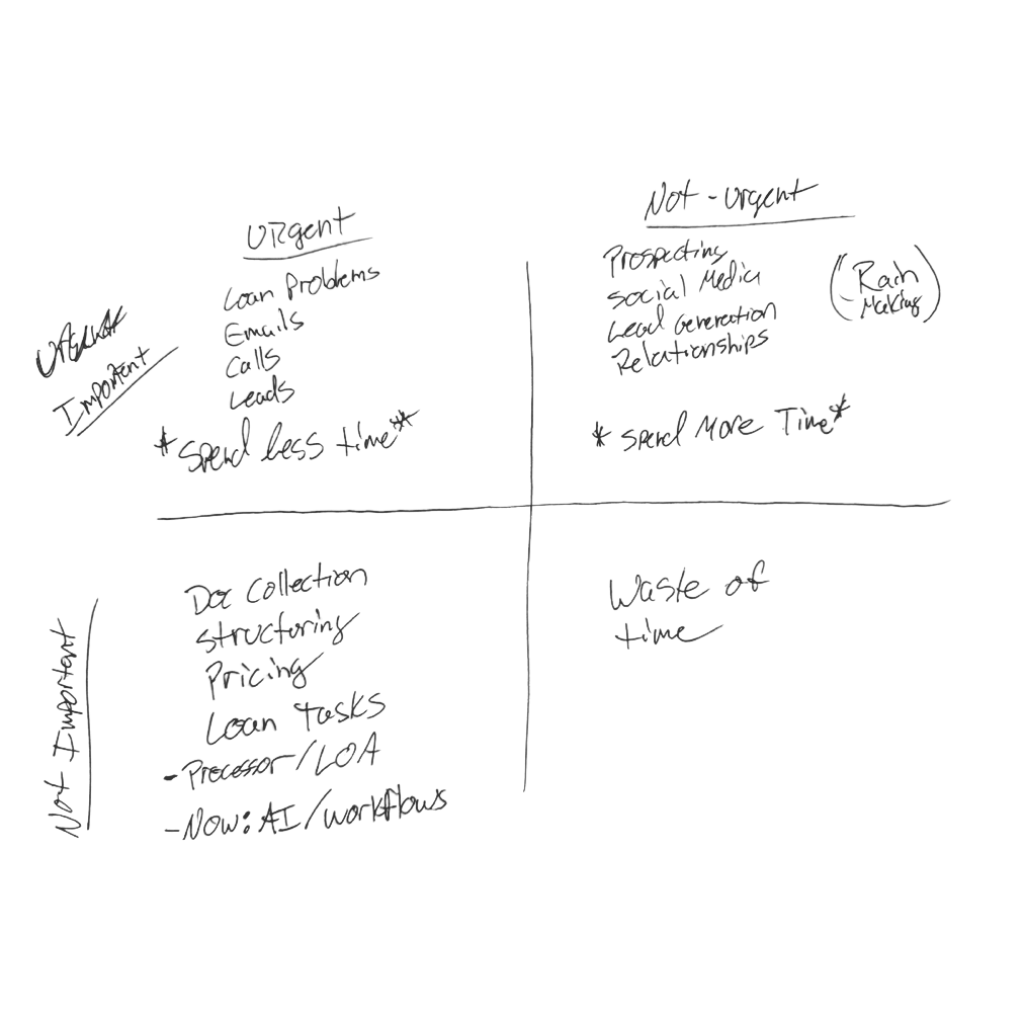

There’s a framework I’ve been thinking about, the Eisenhower Matrix. It separates work into four categories: important and urgent, not important but urgent, important but not urgent, and neither important nor urgent.

Growth comes from the “important but not urgent” quadrant: prospecting, marketing, and relationship building. The activities that compound over time.

But if you’re like most originators working in the old model, you’re spending your entire day in “important and urgent”—putting out fires, handling borrower calls, giving status updates, solving problems. The hard work. The kind that feels productive because it’s exhausting.

I’m not here to tell you that hard work is wrong. It isn’t. But I am here to ask you a question: What if the thing that feels most productive is actually the thing that’s keeping you from growing?

If the systems you work within require you to spend three hours a day communicating about loan status, that’s three hours you’re not spending building your business. And no amount of hustle can make up for structural disadvantages.

What Can You Do About It?

The future, I believe, belongs to originators who find ways to get their time back, not through working less, but through working in systems intelligent enough to remove the nonsense.

And I think what’s going to happen is that companies that free originators up to go to market and sell are the ones that will attract the best people. The companies that can help their originators build personal brands. That can turn them from anonymous processors of paperwork into recognized experts in their markets.

Fame, after all, has a commercial value that’s hard to measure but impossible to ignore. To be known—genuinely known—in your market is worth more than any lead-buying program or CRM system. But building that kind of recognition takes time. Time that most originators don’t have because they’re trapped in systems that steal it from them.

The question worth asking yourself is this: In five years, will you be known in your market? Will people come to you because they’ve heard of you, because they’ve seen your work, because you’ve built something that compounds? Or will you still be chasing the same referrals, working the same grind, hoping the market gets better?

The elephants can’t dance. But that doesn’t mean you can’t.

—Rich

Love this!